If you look up credit on Google, you’ll get a similar definition to “Credit is the ability to borrow money or access goods or services with the understanding that you’ll pay later.”

In personal finance, credit can be described as the money borrowed to you under agreement from a lender or creditor for repayment (1) at a future date along with (2) fees and/or interest. All of the terms of the agreement must be provided in writing and will require a signature from both parties.

Types of Credit

Credit can take on many forms, like personal loans targeted to specific needs (home, auto, student, medical, etc) or credit cards. There are also two credit options that can be drawn on your home which include a home equity loan and home equity line of credit (HELOC).

In general, there are four common forms of credit:

- Revolving Credit: This includes your major credit card accounts

- Charge Cards: This includes

- Installment Credit

- Non-Installment Credit

Credit Score

Your credit score is a representation of your creditworthiness – how likely you are to pay back your financial obligations to lenders. This score will fall between 300 and 850. The higher your score, the more creditworthy you are to lenders. It is an important number to know when taking on new credit (or debt). It can also be useful to landlords when evaluating a new tenant.

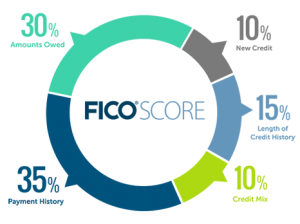

The below image shows six categories used by FICO to determine your FICO score – one type of credit score. More than 90% of lenders use FICO scores to determine your credit risk. This is because it creates an industry standard to evaluate potential borrowers with. The three credit bureaus (Experian, Equifax and TransUnion) maintain a credit report for all potential borrowers in the US with a credit history, which can be supplied to lenders for evaluation. When a lender pulls your credit report, this creates a hard inquiry in your file, showing other creditors that you may be shopping for credit. Pulling your own credit history will not result in a hard inquiry on your file and will not show up on your credit report.

Factors to Consider When Looking into New Sources of Credit

Ultimately, credit is money that you do not own and will need to pay back, so a cost/benefit analysis (Does the benefit of borrowing the money outweigh the cost?) is important, along with determining if you have a reliable means to pay back the full amount owed in the timeframe agreed upon.

There are typically several factors decided on between a lender and borrower that can help you with this:

- Amount borrowed: In financial terms, this is called the principal. This is the amount you will receive from the lender. (Tip: Be careful to read the fine print since some lenders will subtract fees, like origination cost, from this amount, so you will receive the principal minus fees owed.)

- Interest Rate: This is the cost of borrowing the money. I will cover this in length in a later post – there is so much to keep in mind regarding this!

- Term: What is the agreed timeframe that you will take to pay back the full amount.

Are you looking into new forms of credit? In general, it is best to keep your debts low in order to avoid paying interest and be able to manage payments due to creditors.

To get your 3-bureau credit report and get started on managing your credit health, sign up for a free account on Experian.com.

There are many resources online to learn about and review credit card and loan options. Two that I enjoy are CreditKarma and NerdWallet.